Students can Download Chapter 4 Bank Reconciliation Statement Questions and Answers, Plus One Accountancy Chapter Wise Questions and Answers helps you to revise the complete Kerala State Syllabus and score more marks in your examinations.

Kerala Plus One Accountancy Chapter Wise Questions and Answers Chapter 4 Bank Reconciliation Statement

Plus One Accountancy Bank Reconciliation Statement One Mark Questions and Answers

Plus One Accountancy Bank Reconciliation Statement Question 1.

A bank reconciliation statement is prepared with the balance

(a) Passbook

(b) Cashbook

(c) Both pass book and cash book

(d) None of these

Answer:

(c) Both pass book and cash book

Plus One Accountancy Chapter 4 Questions And Answers Question 2.

Passbook is a copy of

(a) Copy of customers account

(b) Bank column of cash book

(c) Cash column of cash book

(d) Copy of receipts and payments

Answer:

(c) Copy of customers’ accounts.

Bank Reconciliation Statement Problems And Solutions Question 3.

………… is a statement showing the causes of the difference between the cash book and passbook balance.

Answer:

Bank Reconciliation statement.

Bank Reconciliation Questions And Solutions Question 4.

Bank Reconciliation Statement is prepared by ………….

Answer:

Businessman/Debtor/Account holder

Bank Reconciliation Statement Problems And Solutions Pdf Question 5.

Credit balance in the passbook means a/an ………… to the depositor.

Answer:

Asset

Bank Reconciliation Statement Questions And Answers Question 6.

Normally, the cash book shows a ………. balance, passbook shows …………. balance.

Answer:

Debit, Credit

Bank Reconciliation Statement Questions Question 7.

Favourable balance as per the cash book means …………… balance in the bank column of the cash book.

Answer:

Debit

Plus One Accountancy Bank Reconciliation Statement Two Mark Questions and Answers

Bank Reconciliation Questions For Class 11 Question 1.

What is a Bank Reconciliation Statement?

Answer:

A statement prepared to reconcile the bank balance as per cash book with the balance as per passbook or bank statement, by showing the items of difference between the two accounts. By the preparation of bank reconciliation statement, one of the balances (either the cash book balance or passbook balance) may be equalized with the other.

Bank Reconciliation Statement Questions And Answers Pdf Question 2.

State the need for the preparation of bank reconciliation statement.

Answer:

It is generally experienced that when a comparison is made between the bank balance as shown in the firms cash book, the two balances do not tally, to reconcile (tally) the two balances of cash book and passbook, bank reconciliation statement is prepared.

Plus One Accountancy Bank Reconciliation Statement Five Mark Questions and Answers

Bank Reconciliation Statement Solutions Question 1.

From the following particulars, prepare the Bank Reconciliation Statement of Asha & Co. as on 31.3.2012.

- Credit balance as per passbook is Rs. 10,000.

- Bank collected a cheque of Rs. 500 on behalf of Asha & Co. but wrongly credited it to Asha’s account.

- Bank recorded a cash book deposited of Rs. 1589 as Rs. 1598.

- Withdrawal column of the passbook undercast by Rs.100.

- The credit balance of Rs. 1500 as on the passbook was recorded in the debit balance.

- The payment of a cheque of Rs. 350 was recorded twice in the passbook.

- The passbook showed a credit balance for a cheque of Rs. 1000 deposited by Asha & Co.

Answer:

Bank Reconciliation Statement as on 31.3.2012

Bank Reconciliation Statement Class 11 Question 2.

The cash book of Reji showed a debit balance of Rs. 4,900 on may 31,2009. On comparing the cash book with a passbook, the following were found.

- Cheques deposited into bank for collection, but not collected till date Rs. 720.

- Cheques issued, but not paid by bank Rs. 650.

- Direct payment by a customer to the bank not recorded in cash book Rs. 520.

- Interest on deposit credited in passbook Rs. 310. Discounted bill dishonoured, entered on in the passbook Rs. 400.

- Bank charges debited in passbook Rs. 75. Prepare Bank Reconciliation Statement of Reji as on May 31, 2009.

Answer:

Bank Reconciliation Statement of Reji as on 31/05/09

Bank Reconciliation Statement Problems Question 3.

The Bank overdraft of Smith Ltd. on December 31, 2010, as per cash book is Rs. 18,000. From the following information, ascertain the adjusted cash balance and prepare bank reconciliation statement.

Rs.

- Unpresented cheque 6000

- Uncleared cheque 3400

- Bank charges debited in the passbook only 1000

- Bill collected and credited in the passbook only 1600

- Cheque of Biju traders dishonored 1000

- Cheque issued to Varma & Co. not yet entered in the cash book 600

Answer:

Adjusted Cashbook (Bank column)

Bank Reconciliation Statement Questions And Answers Class 11 Question 4.

Prepare Bank Reconciliation Statement of Mr. Syam on 31, March 2009 from the following details.

- On 31/3/2009 his passbook show a credit balance of Rs. 1,150 Which was different from his cash book balance.

- On comparison it was found that the cheque of Rs. 1,500 issued on 27th March was paid by the bank oh 4th April.

- Cheques amounting to Rs. 1,700 were deposited . on 28th March but in the passbook only Rs.

700 was credited. - A customer made direct deposit in the bank on 31st March amounting to Rs. 500, this was not recorded in the cash book.

- A discounted bill receivable of Rs. 700 was returned dishonored to the bank on 29th March. This entry was made in the cash book on 3rd April.

Answer:

Bank Reconciliation Statement of Mr. Syam as on 31/03/09

Questions On Bank Reconciliation Statement Question 5.

Balance as per passbook of Mr Kumar is 3,000.

- Cheque paid into bank but not yet cleared. Ram Kumar ₹1,000 Kishorekumar ₹500 1

- Bank charges ₹300

- Cheque issued but not presented Hameed₹2,000 Kapoor₹500

- Interest entered in the passbook but not entered in the Cashbook ₹100

Prepare a bank reconciliation statement.

Answer:

Bank reconciliation Statement of Mr Kumar as on …………

Bank Reconciliation Problems And Solutions Question 6.

The passbook of Mr Mohit current account showed a credit Balance of ₹20,000 on dated December 31, 2005. Prepare a Bank Reconciliation Statement, with the following information.

- A cheque of ₹400 drawn on his saving account has been shown on the current account.

- He issued two cheques of ₹300 and ₹500 on December 25, but only the 1st cheque, was presented for payment.

- One cheque issued by Mr. Mohit of ₹ 500 on December 25, but it was not presented for payment whereas it was recorded twice in the cash book.

Answer:

Bank Reconciliation Statement of Mr Mohit as on December 31st, 2010

Question 7.

On 1st January 2010, Rakesh had an overdraft of ₹8,000 as showed by his cash book. Cheques amounting to ₹2,000 had been paid in by him but were not collected by the bank by January 1, 2010.

He issued cheques of ₹ 800 which were not presented to the bank for payment up to that day. There was a debit in his passbook of ₹60 for interest and ₹100 for buffet charges. Prepare bank reconciliation statement for comparing both the balance.

Answer:

Bank Reconciliation Statement of Mr Rakesh as on 1st January 2010.

Question 8.

Prepare bank reconciliation statement.

- Overdraft shown as per cash book on December 31, 2010, ₹10,000.

- Bank charges for the above period also debited in the passbook, ₹100.

- Interest on overdraft for six months ending December 31, 2010, ₹380 debited in the passbook.

- Cheques issued but not encashed prior to December 31, 2010, amounted to₹2,150.

- Interest on Investment collected by the bank and credited in the passbook, ₹600.

- Cheques paid into bank but not cleared before December31,2010were₹1,100.

Answer:

Bank Reconciliation Statement as on 31st December, 2010.

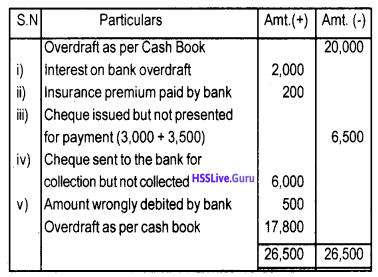

Question9.

Prepare a bank reconciliation statement from the following particulars and show the balance as per cash book.

- Balance as per pass book on December 31, 2010, overdrawn₹20,000.

- Interest on bank overdraft not entered in the cash book ₹2,000.

- ₹200 insurance premium paid by bank has not been entered in the cash book.

- Cheques drawn in the last week of December 2010, but not cleared till date for ₹3,000 and ₹3,500.

- Cheques deposited into bank in November 2010, but yet to be credited on dated December 31, 2010, ₹6,000.

- Wrongly debited by bank, ₹500.

Answer:

Bank Reconciliation Statement as on 31st March, 2010

Plus One Accountancy Bank Reconciliation Statement Eight Mark Questions and Answers

Question 1.

What are the various reasons for the difference between balance as per cash book and passbook?

Answer:

There are several reasons that contribute for the disagreement of the balance as shown by cash book and passbook. They are as under:

1. Cheques issued but not presented for payment:

When the trader issues a cheque, he credits its amount immediately in his cash book. The same will be entered in the passbook only on presenting the cheque and making payment by the bank. If the cheque is not presented for payment before the date of preparation of bank reconciliation statement, the balance as per Pass Book will be more than the balance as per Cash Book.

2. Cheque paid in for collection but not collected:

On deposition cheques into the bank for collection, the trader debits the same amount in the bank account. The bank credit the amount in the passbook only on getting the amount collected. Such uncleared cheques make the cash book balance to be more than the passbook balance.

3. Direct payment by a customer to the bank:

Customers of the trader occasionally make some payments directly into the trader’s bank account. The trader may come to know of an only later. But the banker gives immediate credit to the trader on receipt of the amount. If it remains unrecorded in the cash book, the balance as per pass book will be more than the balance as per cash book.

4. Interest on deposit credited by the banker:

At regular intervals, banks allow interests on the deposit balance of the trader and credit the amount in the passbook. The same usually remains unrecorded in the cash book. In such a case, the passbook balance will be more than the cash book balance.

5. Interest, dividend, rent, etc. collected by bank:

Bank collects interest, dividend, rent, etc. on behalf of the customer and credits the same to his account. The trader comes to know of it only on a later date. If such collection remains unrecorded in the cash book, the passbook balance will be more than the cash book balance.

6. Payment made on behalf of the customer:

The banker makes payment for rent, insurance, etc., for the customer as per standing instructions. The banker debit the trader’s account with such payments. The trader comes to know of it only later. Due to such payments that remain unrecorded in cash book, the balance as per pass book will be less than the balance as per cash book.

7. Bank charges as per Pass Book:

Bank charges and commission for collection of cheques, bills, etc., are debited in the passbook. The corresponding credits are often not given in the cash book. As these items are not entered in the cash book, its balance will be more than that of the passbook.

8. Bills Receivable discounted, but dishonored:

When a trader discounts bills of exchange, the banker credits the trader’s account with the amount due. The same amount is debited by the trader in cash book. If such a bill is later dishonored, the banker immediately debits it in the passbook. But the same remains unrecorded in the cash book. This cause the balance as per cash book to be more than the passbook balance.

9. Interest on overdraft debited in passbook:

Periodically the bank calculates interest due by the trader on his overdraft and debits the amount in the passbook. Corresponding credit is often not made by the trader in his cash book. It leads to difference in the balance as per cash book and passbook.

10. Credit instruments credited by bank but not recorded in cash book:

Bills of exchange, promissory notes and other credit instruments collected by bank are credited in the passbook. But if they remain unrecorded in the cash book it may lead to disagreement between the balance as per the two books.

11. There may also be instance of cheque recorded as paid in for collection but failed to be deposited into the bank, by which the cash book balance will be more than the balance as per passbook.